One of the most influential lines of research on income inequality come from Thomas Piketty and Emmanuel Saez’s study of income tax records in the United States and elsewhere. Summarizing this work in Slate, Timothy Noah states:

“The share of national income going to the top 1 percent (the Rich) more than doubled during the Great Divergence [the last 30 years] and now stands at about 21 percent…” [and] “the share of national income going to the top 0.1 percent (the Stinking Rich) increased nearly fourfold during the Great Divergence.”

In a new NBER working paper, Philip Armour and colleagues dispute the Picketty and Saez interpretation of income inequality. Income inequality has increased in some respects, they argue, but much more slowly than previous analysis suggests. This new paper picks up where their prior work left off (see my summary here).

The new paper provides lots to think about conceptually and empirically – some things which I agree with, some which I would debate, but lots which I frankly cannot comment on for lack of expertise. Readers, if this is your field of study, please provide comments and clarification, and I’ll try to follow-up.

How to Measure Income

There are lots of decisions about how to count income – should we measure it before taxes or after? How should we value government transfers and subsidies? What is the right way to measure capital gains?

What we want in an income measure is a way of accounting for the change in the set of resources that a household has available for consumption from year to year (remember, income is a measure of flow and wealth is a measure of stock of total assets). The authors argue for the Haig-Simons definition of income, which states that income is the “the money value of the net accretion to one’s economic power between two points of time.” This definition makes a big difference in the measurement of capital gains, which greatly affects top share income growth measurement:

“[Haig-Simons] includes capital gains at accrual, measured as the increase or decrease in the value of capital assets in each year regardless of whether that asset was sold for a taxable realized gain. In contrast, taxable realized capital gains include asset appreciation that may have occurred years or decades earlier as current income. This is because individuals can choose, through the timing of transactions, when to realize capital gains for tax purposes”

The income value of your Apple stock in any given year is whatever that stock gained on the market, whether or not you cashed it in. Alternatively if you do cash in your stock this year some of the value you realize should be imputed to previous years when the asset increased in worth. As a matter of accounting, this seems right to me.

A Long Sidebar on Health Insurance…

As I’ll illustrate in a minute, changing the accounting of capital gains makes a big difference at the top of the income distribution. In the middle and the bottom, accounting for the value of government transfers and fringe benefits dramatically changes the picture (they made this point in the previous paper too).

The big issue here is health insurance. How much should we say health insurance adds to a household’s income? The conventional method is to impute a “fungible value” – the amount of money a household would have spent on health care if the government had not paid for it. This is mainly what the Census Bureau does. As the authors summarize:

“The ex-ante value for Medicare and Medicaid is calculated as the respective program’s average outlay by state and risk class in the income year in question. For higher income individuals, the Census Bureau values insurance as this ex-ante value, just as was the case for employer-provided insurance. But for families that cannot meet basic food and housing requirements, the Census Bureau assumes that the family derives no value from the insurance, because the government provision of insurance frees up no income to be otherwise spent to purchase insurance on their own. This approach implicitly assumes that since such families cannot afford their basic needs, they would be unlikely to purchase this insurance at any price.”

They reject this method:

“Simply because low-income individuals would forego insurance, if it were not provided to them, does not indicate that they receive no value from it. Rather it implies that their consumer surplus from its purchase is less than the consumer surplus from other purchases, given the same level of spending.”

But consumer surplus is not exactly the issue here. The issue is how much consumption is increased by health insurance. We actually don’t exactly know how much getting health insurance increases consumption opportunities for low-income families, although there are some studies that try to indirectly address this issue (I have looked at a related issue in a recent paper). In general, many uninsured families consume some health care, but the amount on average is modest. They mostly postpone healthcare in order to pay for housing and other necessities.

Having health insurance is clearly of value for low-income households (a point that the study authors hasten to emphasize too), but that value does not necessarily get reflect in an income measurement perspective. For income measurement, we should remain neutral about whether families derive additional non-consumption value from various in-kind goods. Lots of the good things about health insurance (risk protection, access to lifesaving medical services, and so forth) are not income, and should not be measured as such.

Capital Gains

They estimate two kinds of capital gains. Realized capital gains – the amount of money that is actually taken in from the stock market in the year – are estimated from household data that are adjusted for top-coding:

“Among imputed filers in the CPS data, we again rank tax units by taxable income into percentiles. We perform a similar ranking on the IRS tax return data for each year. We then input the taxable realized capital gains for each tax unit in the CPS data as the mean taxable realized capital gains for tax units in the same percentile of the taxable income distribution in the tax return data, assuming that non-filers have no taxable realized capital gains”

They estimate accrued capital gains – the amount of money that a household has gained from capital investments, whether they realize it or not in the year – by imputing accrued capital gains from stocks as the appreciation in the Dow Jones Industrial Average in the year times the assets held in stocks and mutual funds. (There is some discussion about how well such an index is likely to capture the rates accrual for different types of investors, but I’ll leave that aside for now).

Key Conclusions

Here are some of the main conclusions:

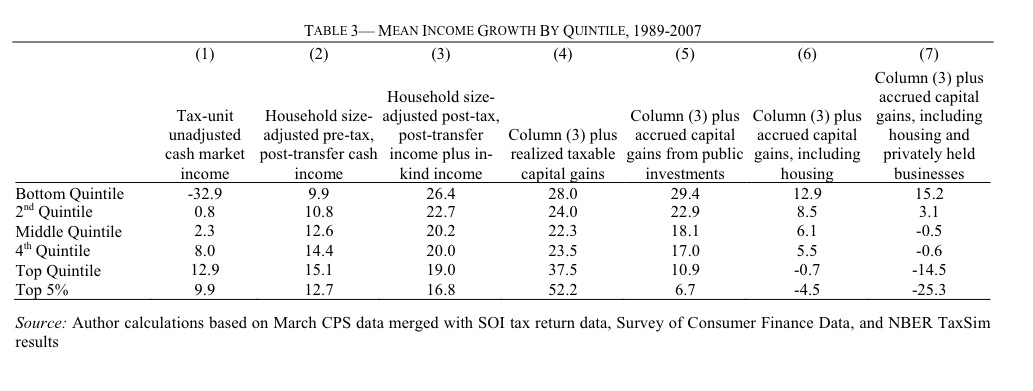

“The inclusion of taxes—because they have fallen as a share of income, especially at higher income levels—and in-kind benefits—because they have risen as a share of income, especially at lower income levels—increases income growth throughout the distribution. But it does so most, among the bottom two quintiles. As a result income growth between 1979 and 2007 is remarkably similar for each of the bottom four quintiles. The top quintile and the top 5 percent continue to grow faster, 54.0 and 68.9 percent respectively (column 3), but the gap in growth between them and the bottom quintile is dramatically smaller than the gap using a Piketty-Saez style cash market income of tax unit measure of income.”

When they include realized capital gains they find that income inequality has grown consistent with the estimates provided by the Census Bureau, however, when they switch to the accrued capital gains perspective, they find a very different story:

“when we include yearly-accrued capital gains excluding housing gains and private business gains, instead of taxable realized capital gains, the inclusion of these gains slows income growth in all but the bottom quintile of the distribution. Thus, when using this measure that is more in line with Haig-Simon’s income principles, the top quintile of the distribution had the least growth in income from 1989 through 2007 while the bottom quintile of the distribution had the most. Measured in this way income inequality fell between 1989 and 2007”

Column 5 versus Columns 1-4 tell the main part of the story here:

Summary Thoughts

This is a complex paper with a clear message: commonly used measures of income inequality are flawed. Beyond the amount on people’s paychecks, we need to account for what people get from the government, what they pay in taxes, and what they are accruing over time in capital wealth (market investments and housing wealth).

This study should be most concerning to scholars and policymakers on the left that make the argument that steps should be taken to rein in income inequality because it has grown substantially over the past three decades. If that is your main view, you should either concede that the argument is now weakened, or you should be able to counter this study’s findings.

Of course, there are still some other positions that this study does not contradict: it is still reasonable to argue that things would have been much worse were it not for taxes and transfers (including government health care, which may be somewhat overstated here anyway). It is also reasonable to argue that inequality in the levels (and not necessarily the trend) is alarming in and of-itself (although they calculate smaller Gini coefficients with their adjusted data). Finally, you could be an inequality skeptic, but still believe that absolute states of deprivation in our society (such as incomes that cannot support reasonable consumption and human capital investment for disadvantaged families) warrant intervention, no matter how much better or worse the best-off are doing in comparison. That’s my view for now.

{kind=link}

2 responses to “Has Income Inequality Really Ballooned Since the 1970s?”

About the “Great Divergance” – it made me think of the question: “Do people become wealthy by virtue or by vice?”. It seems to me that the premise of the GD is that GD occurred (likely) due to some unfair manipulation of the system (UMOTS). Btw, I am someone who believes that there definitely is UMOTS – for what it’s worth. But I also think that it may very well be that the GD happened partly bcz of an earlier divergence in virtue. Here’s what I mean: people at the “top” looked back over their lives in 1970 and said to themselves “hey, all of that studying and learning and researching (SALAR) that I did between 1950 and 1969 has paid off handsomely for me. Therefore I am going to devote even more of my resouces to SALAR in the years ahead.”. Meanwhile the people at the “bottom” just continued doing what they had been doing since the beginning of time – I.e., hand-to-mouth working and consuming. So, 40 years later the group that increased their SALAR “investment” is, understandably, proportionally further ahead than the group which did not.

So I really do believe that one factor that explains the GD is the UMOTS. But, if for philosophical reasons, we ignore the possible roles of variation in virtue beteen groups, then the final perception that we form of the GD might be off target.